The Daily Shot: 11-Jun-24

• The United States

• The Eurozone

• Europe

• Asia-Pacific

• China

• Emerging Markets

• Cryptocurrency

• Commodities

• Energy

• Equities

• Credit

• Global Developments

• Food for Thought

The United States

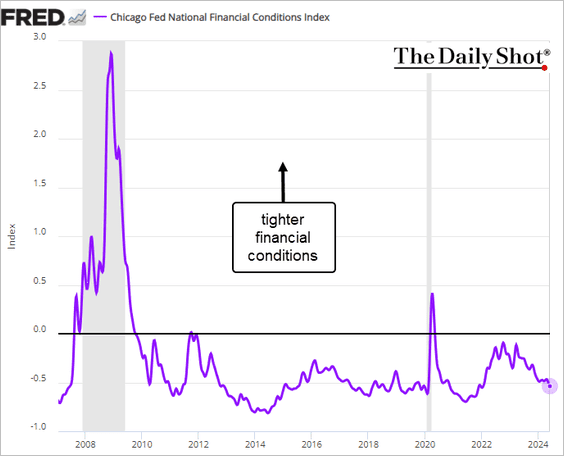

1. US financial conditions continue to ease, further contributing to the Fed’s reluctance to lower rates.

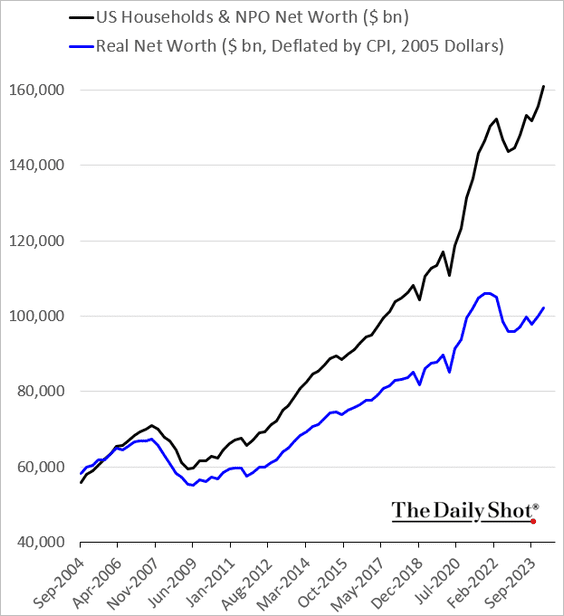

2. Households’ net worth reached a record high in the first quarter, bolstered by a strong stock market and robust cash yields. However, when adjusted for inflation, household wealth remains below its 2021 peak.

Source: @wealth Read full article

Source: @wealth Read full article

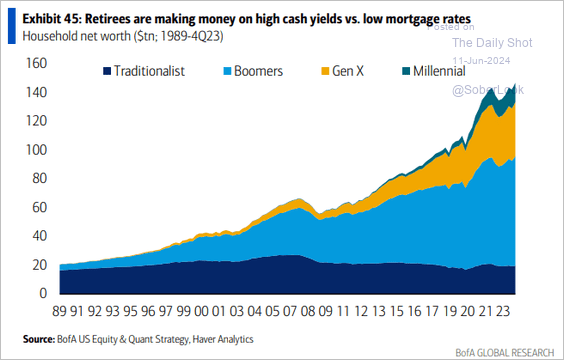

Here is the breakdown by generation.

Source: BofA Global Research; @MikeZaccardi

Source: BofA Global Research; @MikeZaccardi

——————–

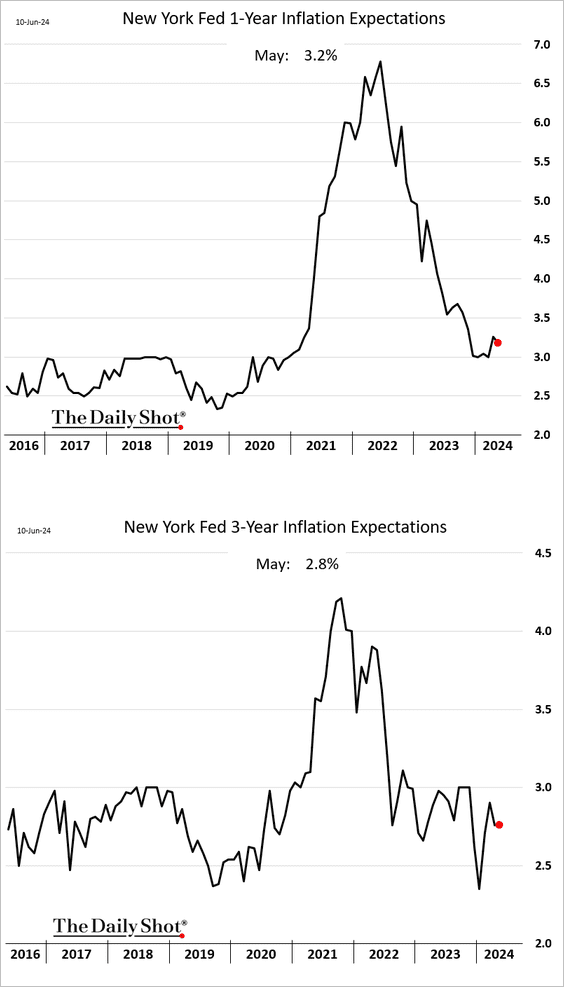

3. Next, we have some updates on inflation.

• According to the NY Fed’s Survey of Consumer Expectations, short-term inflation expectations edged lower last month.

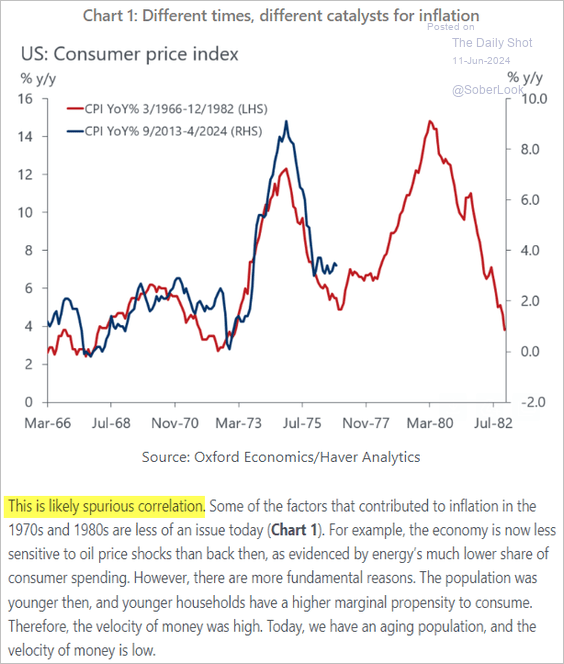

• Are the fears of a second inflation wave overblown? Below is a comment from Oxford Economics.

Source: Oxford Economics

Source: Oxford Economics

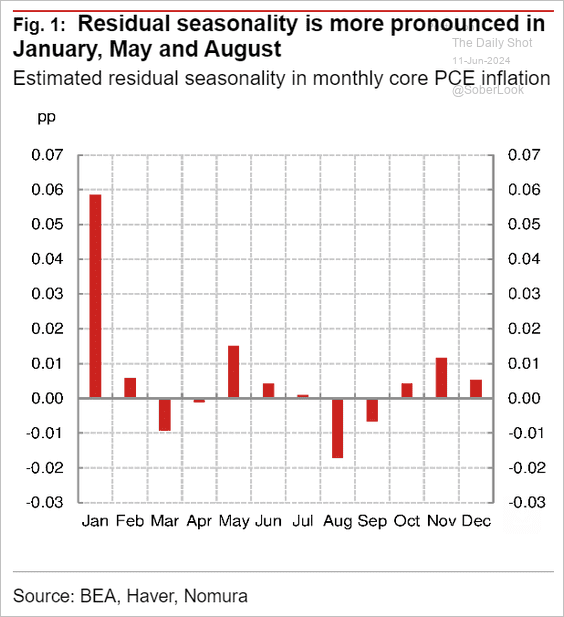

• Seasonal adjustments to PCE inflation don’t fully remove the seasonality. And May tends to exhibit an upside bias.

Source: Nomura Securities

Source: Nomura Securities

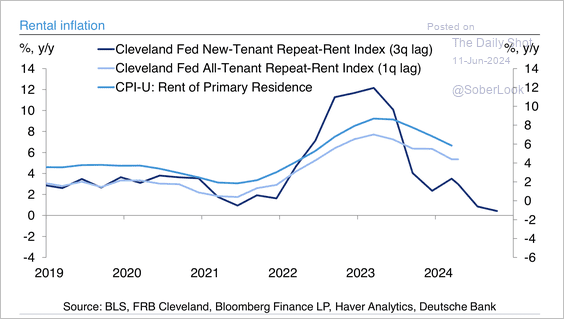

• Leading indicators point to further disinflation in rent prices.

Source: Deutsche Bank Research

Source: Deutsche Bank Research

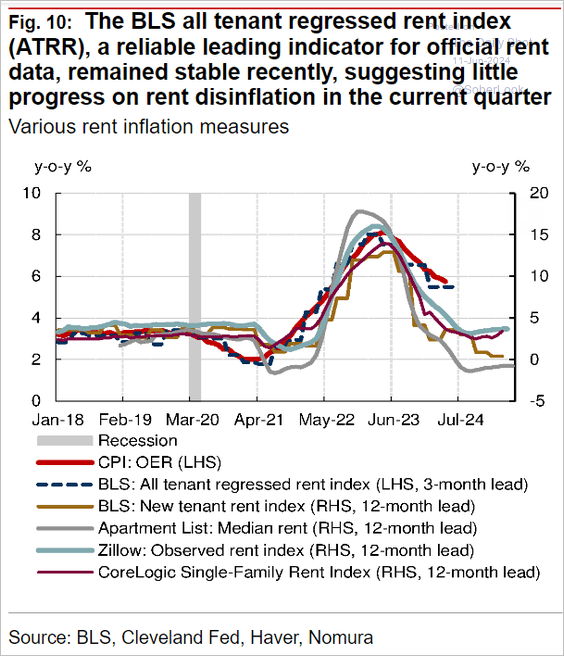

– However, the “BLS all tenant regressed rent index” suggests that rent disinflation has stalled this quarter.

Source: Nomura Securities

Source: Nomura Securities

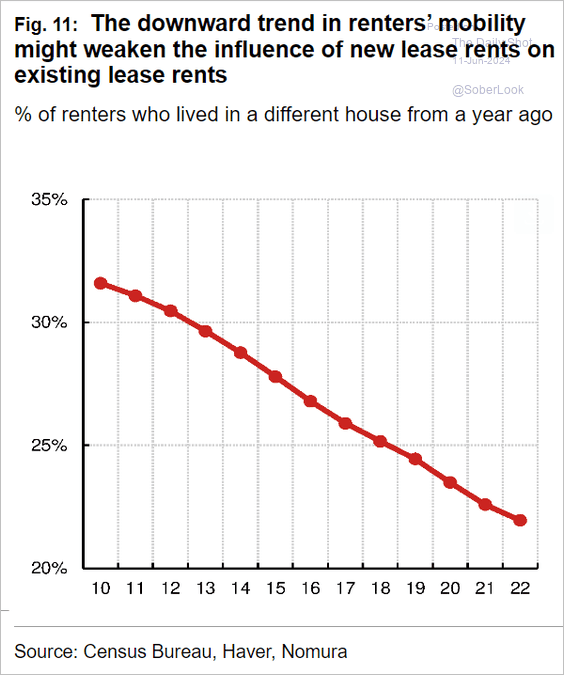

– Renters are moving less frequently in recent years, causing the decline in rent inflation for new rentals to take longer to affect the overall market.

Source: Nomura Securities

Source: Nomura Securities

• Economists continue to be surprised by the persistent stickiness of US inflation. It was initially thought that rapid rate hikes (a 5.25% increase over a year and a half) would slow demand and cap inflation. However, higher rates have unexpectedly contributed to inflation in certain sectors of the economy.

– Housing Market Impact: High mortgage rates have drastically reduced the supply of homes for sale. Homeowners who would typically trade up for larger homes are staying put to maintain their pre-increase 3% mortgage rates, and/or they are unable to afford the much higher rates currently available. This has led to continued increases in home prices, which, combined with high mortgage rates, has severely affected affordability. Poor affordability, in turn, is driving up rent costs and homeowners’ equivalent rent, which constitute a significant portion of the core CPI. Moreover, high borrowing costs have made it more challenging for builders to increase the supply of housing.

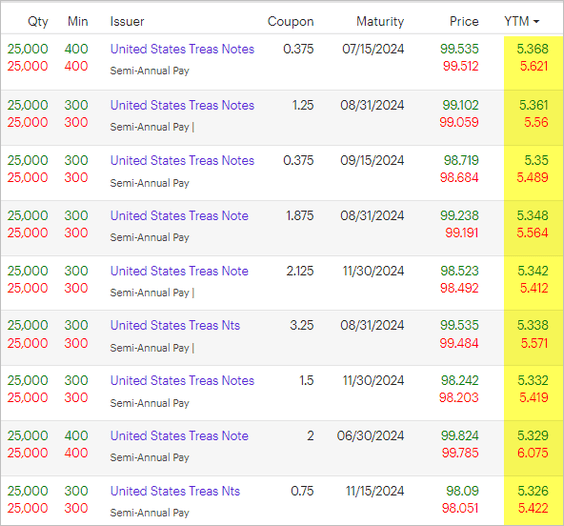

– Savings Disparity: While many lower-income households have depleted their pandemic-era savings and are burdened with credit card debt, upper-income households still hold substantial savings and are less affected by high credit card rates. High short-term rates have allowed these households to generate significant income. For example, here is a look at T-Bill offerings through E-Trade.

Source: E*TRADE

Source: E*TRADE

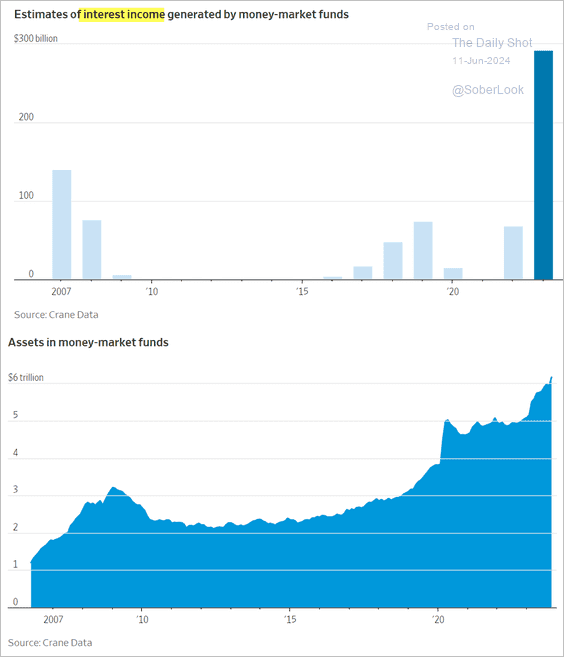

Money market funds are generating record amounts of cash.

Source: @WSJ Read full article

Source: @WSJ Read full article

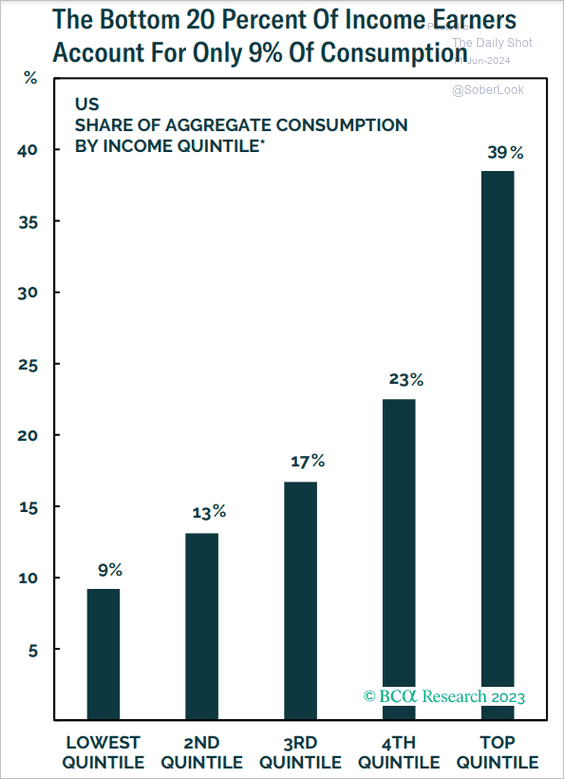

Coupled with record-high stock market levels and robust home prices, upper-income consumers continue to spend despite high rates and elevated prices. Since upper-income households drive much of US consumer spending (as illustrated in the chart below), their continued expenditure boosts demand and hampers disinflation.

Source: BCA Research

Source: BCA Research

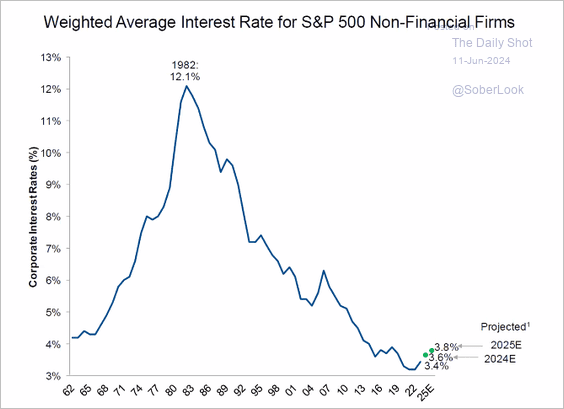

– Corporate Sector Resilience: Many companies secured low financing rates following the COVID shock (see chart below) and have not been significantly impacted by higher rates.

Source: @Maverick_Equity

Source: @Maverick_Equity

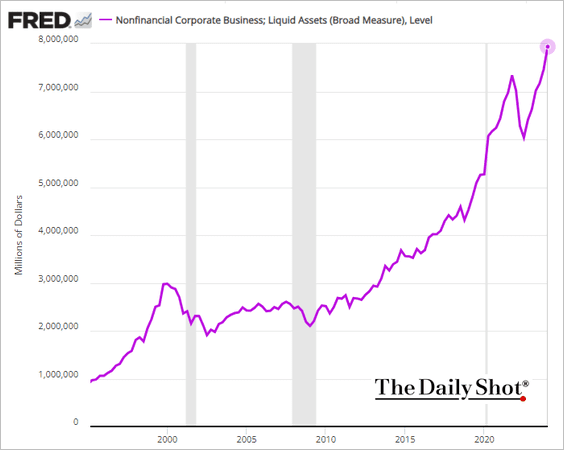

Large firms possess substantial cash balances (see chart below), which, like upper-income consumers, benefit from high rates by generating significant interest income. A large portion of this cash is returned to shareholders, further increasing income for wealthier households. Companies continue to hire, which also increases demand.

The anticipated effects of rapid rate hikes on US inflation have not materialized as expected. Instead of curbing inflation, higher rates have exacerbated it in certain sectors. The housing market, savings disparity, and corporate sector resilience are key areas where higher rates have contributed to ongoing inflationary pressures.

Back to Index

The Eurozone

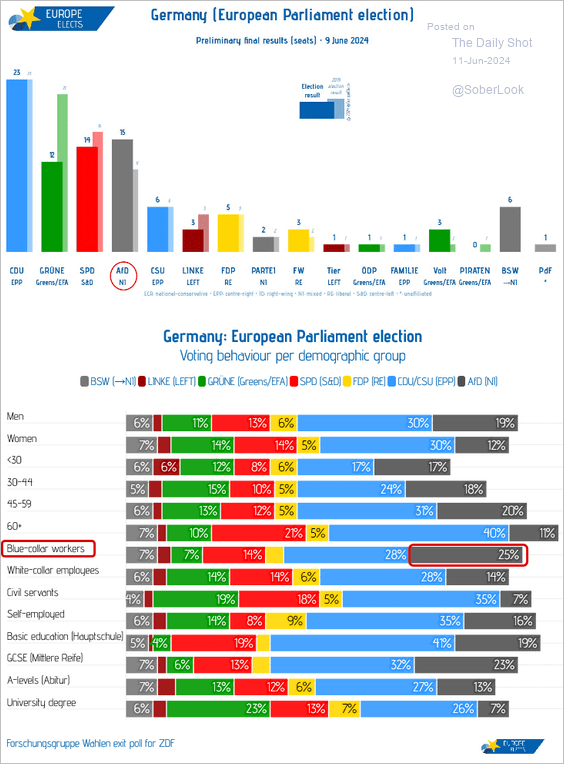

1. The far-right surged in the EU vote, showing strength in Germany, France, and Austria. In Germany, the CDU/CSU (EPP) emerged as the leading party, while the right-wing populist AfD also made gains.

Source: @EuropeElects

Source: @EuropeElects

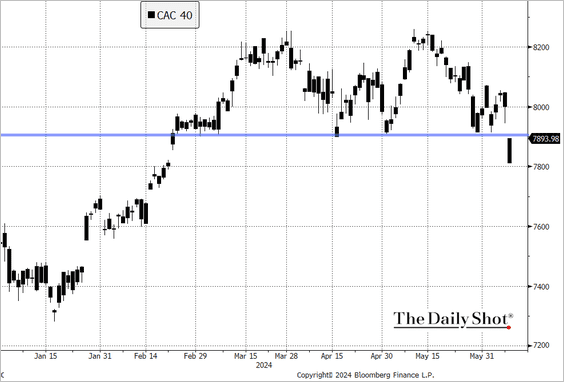

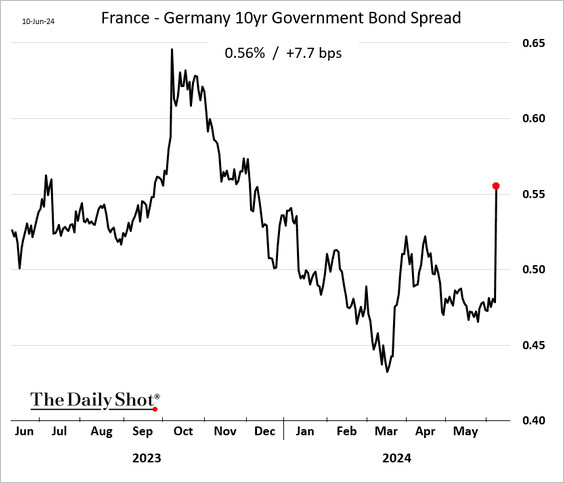

2. The announcement of snap elections in France caused stocks to decline, though the selloff was contained.

The French bond spread to Germany widened.

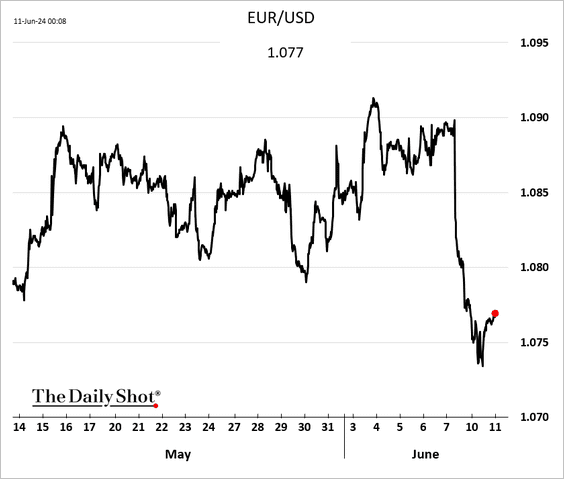

3. The euro appears to have stabilized.

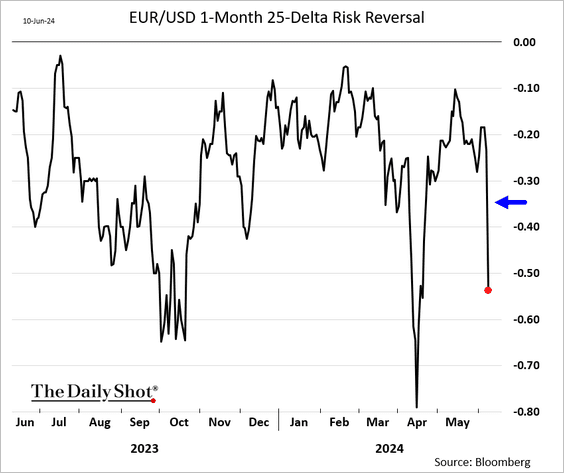

The EUR/USD risk reversals show increased downside bias ahead of the French elections.

——————–

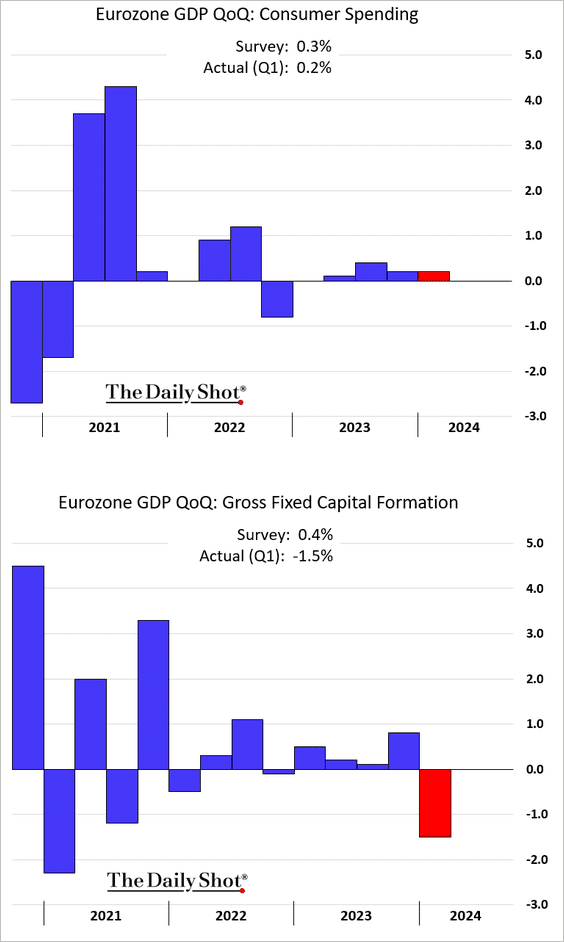

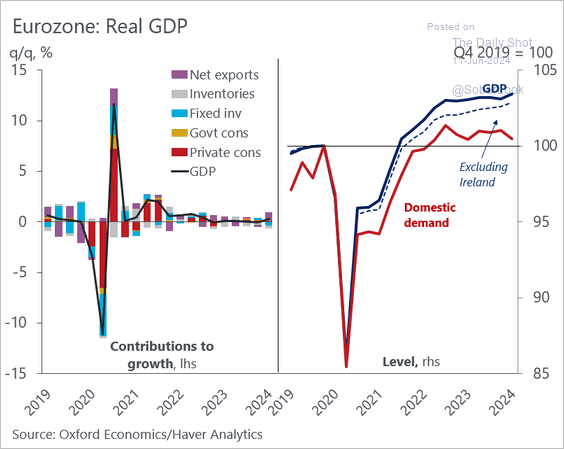

4. Q1 domestic demand in the euro area was weaker than previously estimated.

Source: @DanielKral1

Source: @DanielKral1

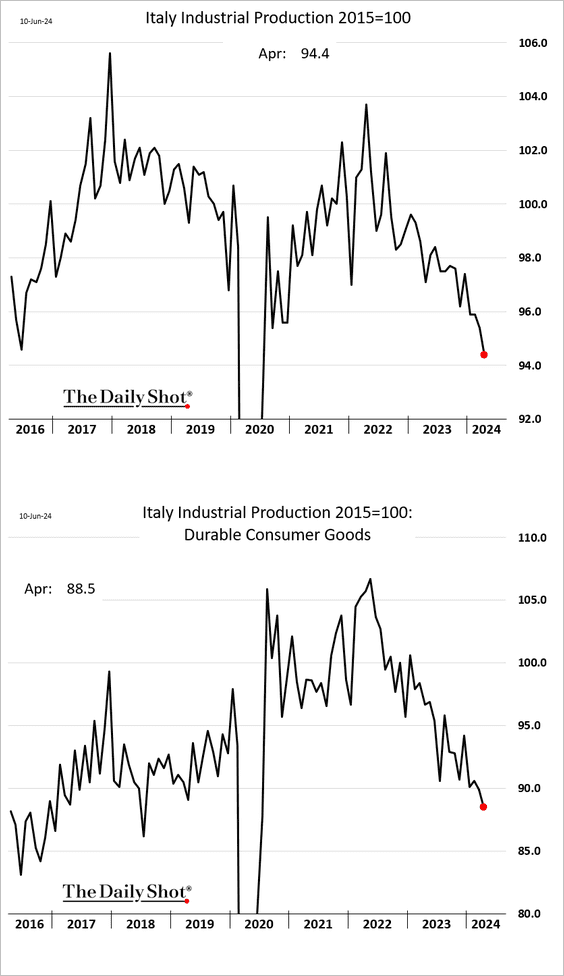

5. Italian industrial output continues to sink.

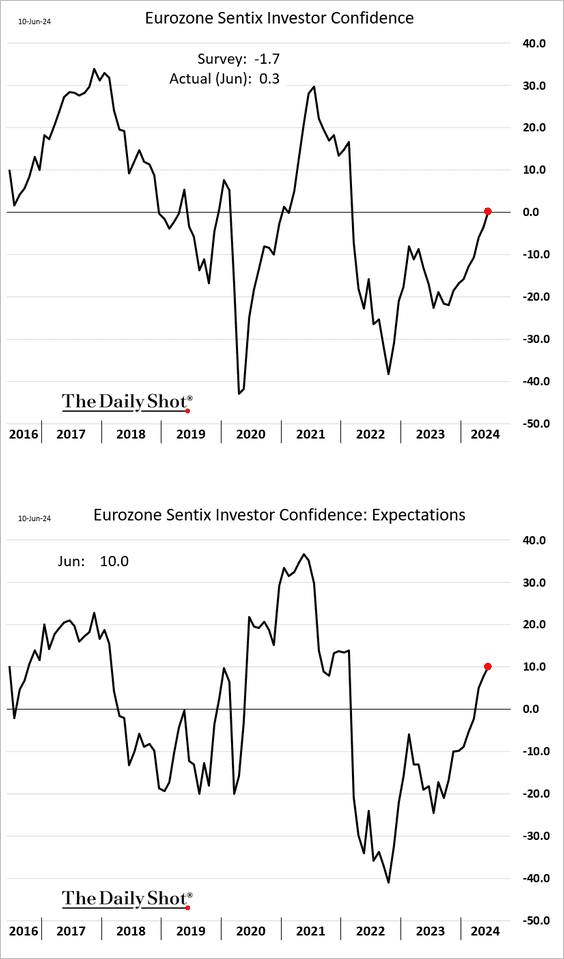

6. Eurozone investor sentiment keeps improving.

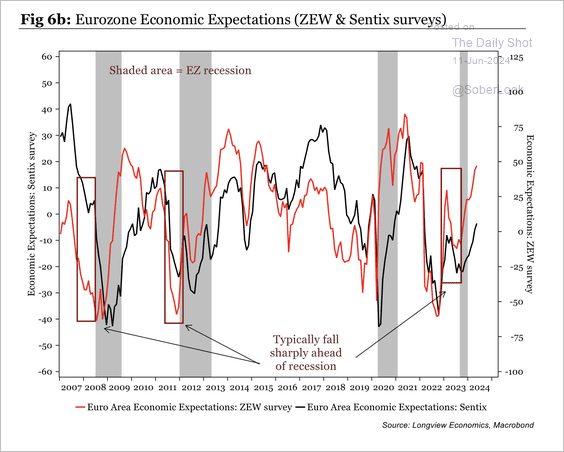

The recent rebound in Eurozone economic expectations is similar to previous recession troughs.

Source: Longview Economics

Source: Longview Economics

Back to Index

Europe

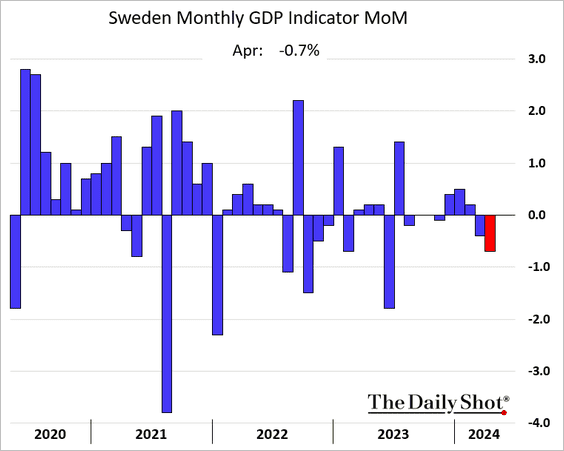

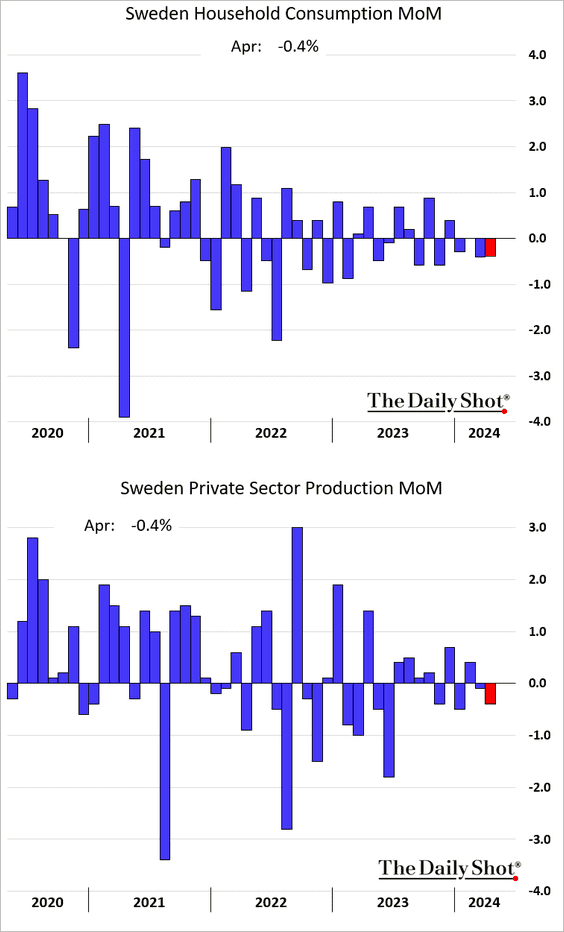

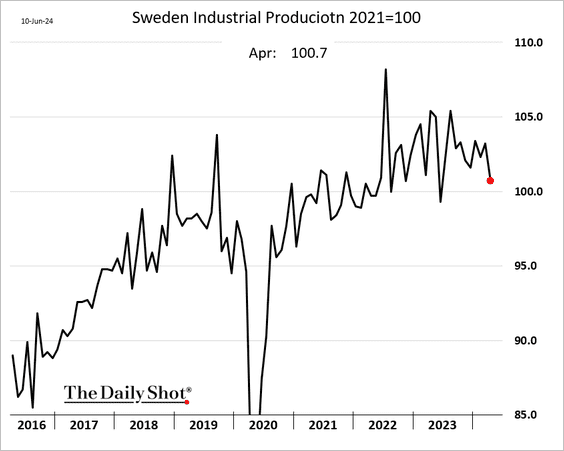

1. Sweden’s monthly GDP estimate declined in April, …

… as economic activity slowed.

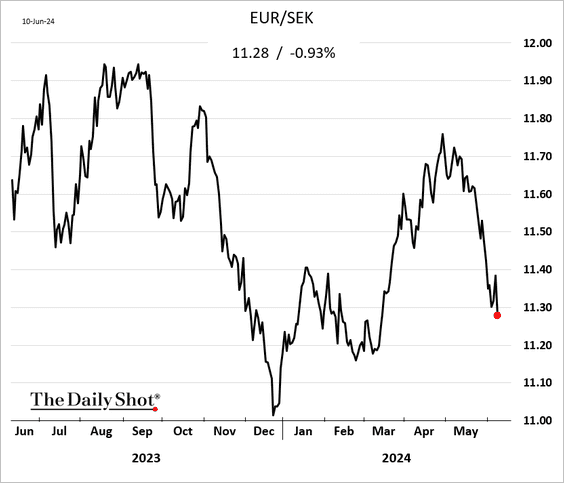

Nonetheless, the Swedish krona has been strengthening against the euro.

——————–

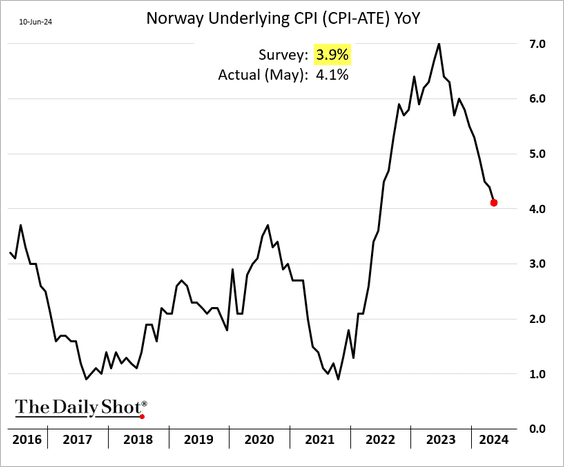

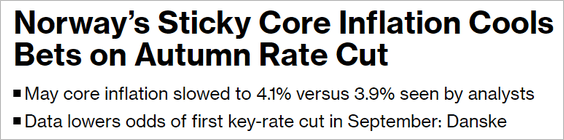

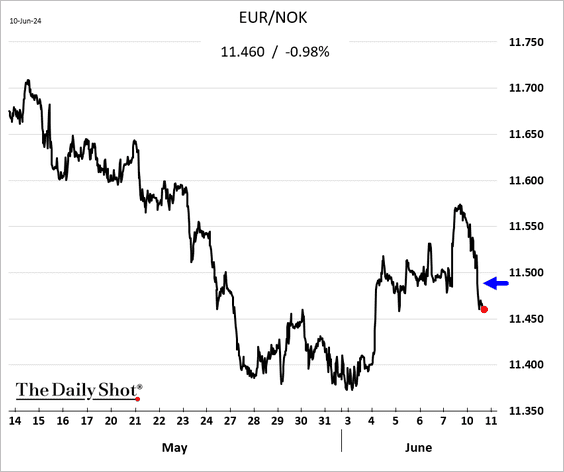

2. Norway’s core inflation was stronger than expected in May.

Source: @economics Read full article

Source: @economics Read full article

• The krone strengthened vs. the euro.

• Bond yields jumped.

Back to Index

Asia-Pacific

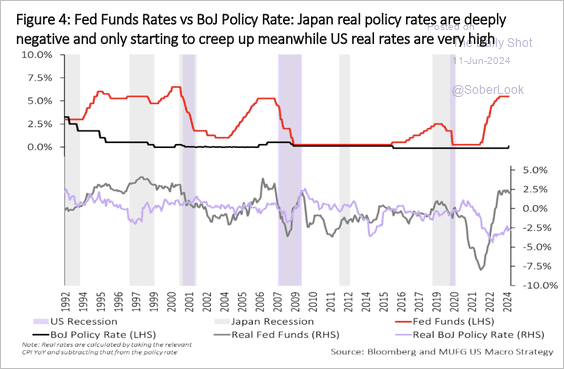

1. The wide gap between US and Japanese real rates could narrow as both nations reverse unconventional monetary policies.

Source: MUFG Securities

Source: MUFG Securities

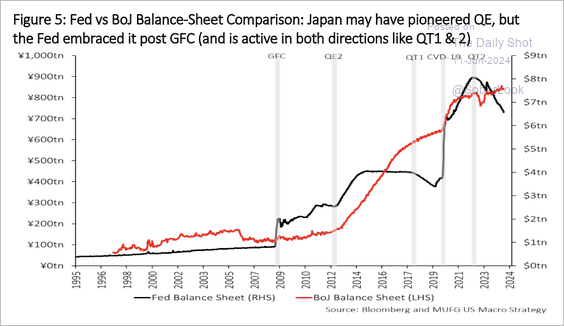

• This chart shows diverging balance sheet dynamics between the BoJ and the Fed.

Source: MUFG Securities

Source: MUFG Securities

——————–

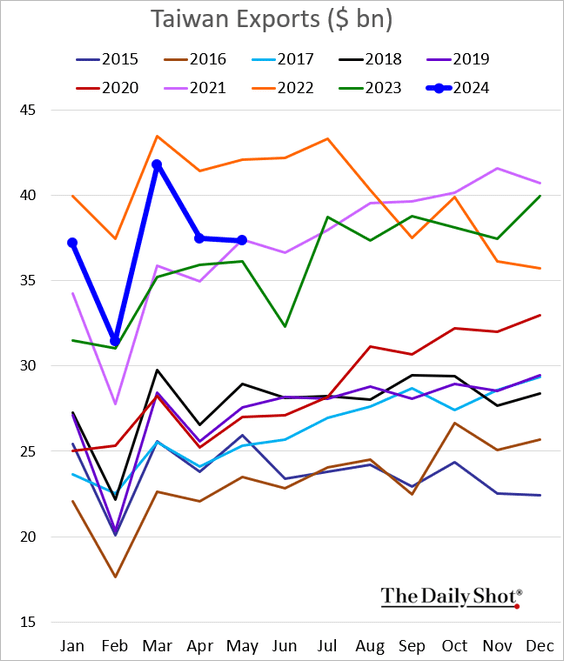

2. Taiwan’s exports were lower than expected in May but still above 2023 levels.

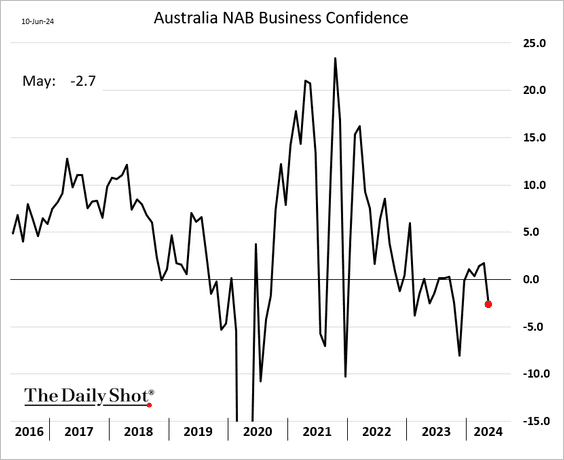

3. Australia’s business confidence declined in May.

Back to Index

China

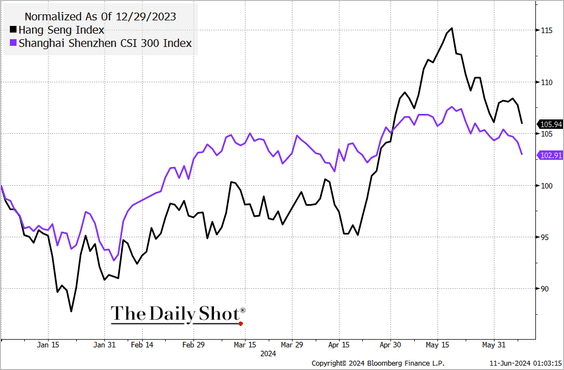

1. The stock market has been rolling over.

Source: @TheTerminal, Bloomberg Finance L.P.

Source: @TheTerminal, Bloomberg Finance L.P.

——————–

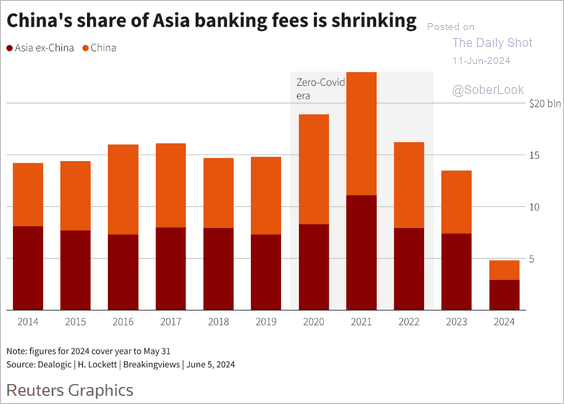

2. Investment banks are struggling to stay profitable in China.

Source: Reuters Read full article

Source: Reuters Read full article

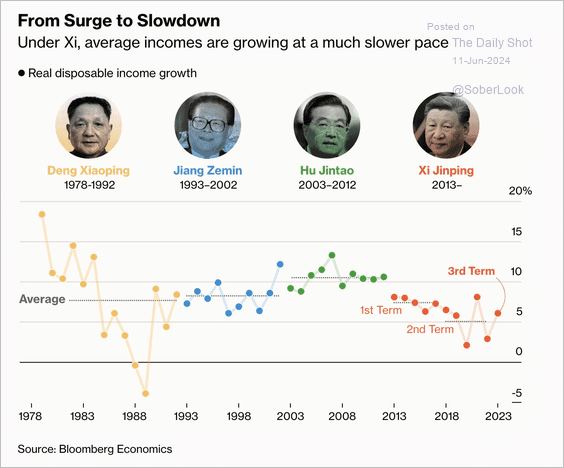

3. Here is a look at real disposable income growth from 1978 to 2023 across different leadership periods.

Source: @business Read full article

Source: @business Read full article

Back to Index

Emerging Markets

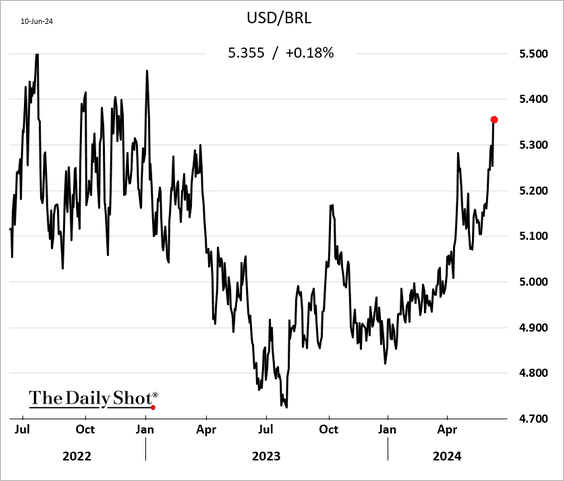

1. The Brazilian real has been selling off, putting downward pressure on some commodities (such as sugar).

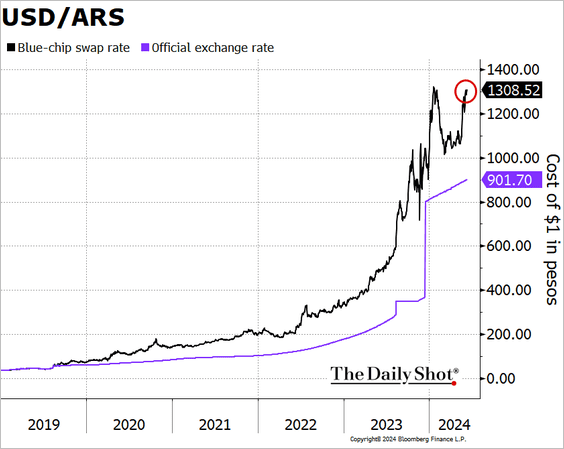

2. The Argentine peso is nearing record lows vs. USD in the “unofficial” markets.

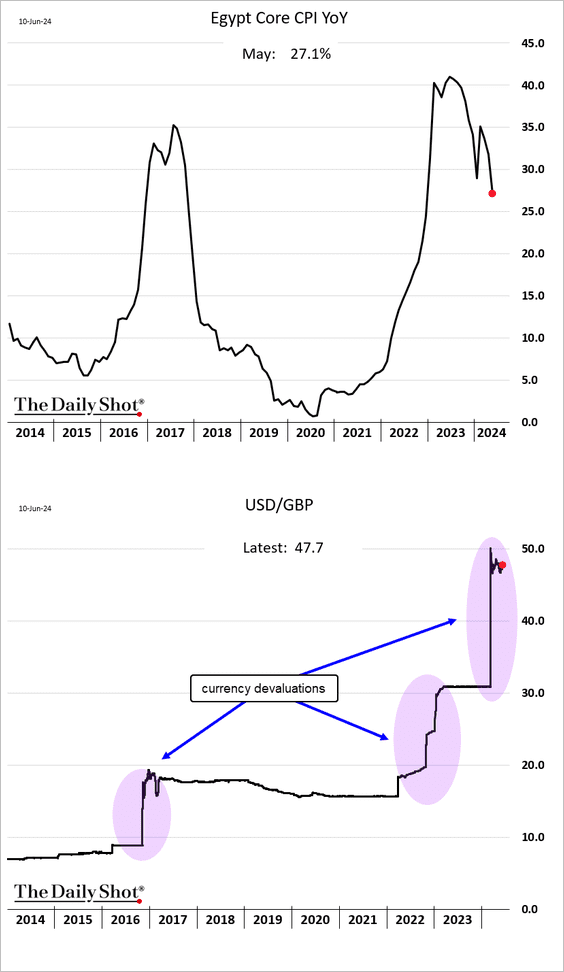

3. Egypt’s CPI is starting to ease as the impact of the latest currency devaluation slows.

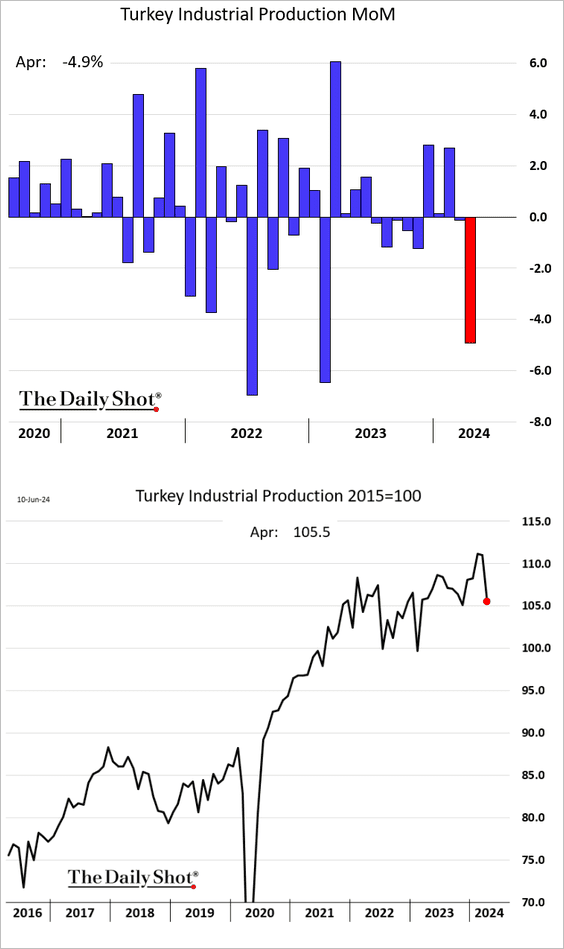

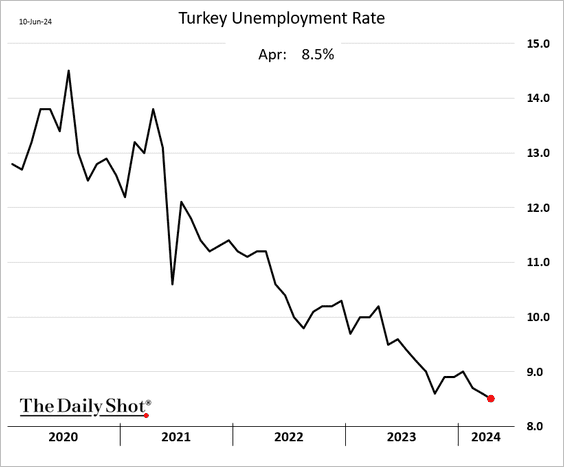

4. Turkey’s industrial production declined in April.

The unemployment rate continues to trend lower.

Back to Index

Cryptocurrency

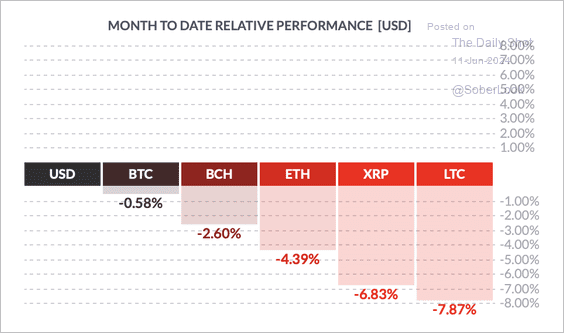

1. Cryptos are off to a weak start this month, with Litecoin (LTC) underperforming top peers.

Source: FinViz

Source: FinViz

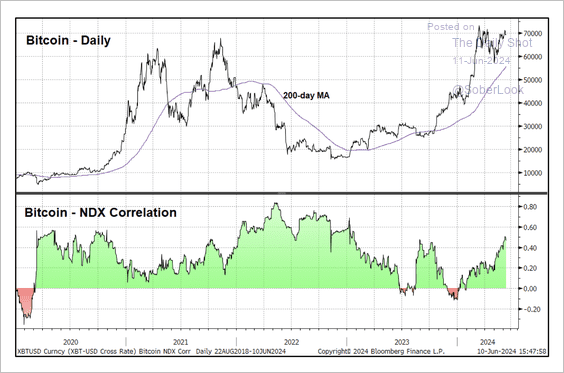

2. Bitcoin’s correlation with the Nasdaq 100 remains elevated.

Source: @StocktonKatie

Source: @StocktonKatie

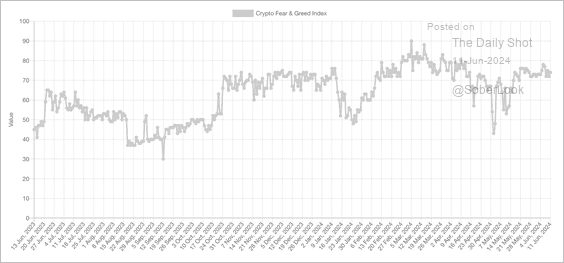

3. The Crypto Fear & Greed Index has remained in “greed” territory over the past two weeks.

Source: Alternative.me

Source: Alternative.me

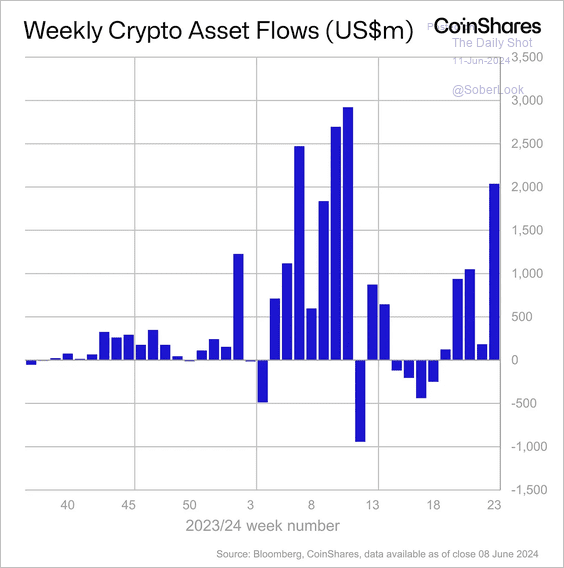

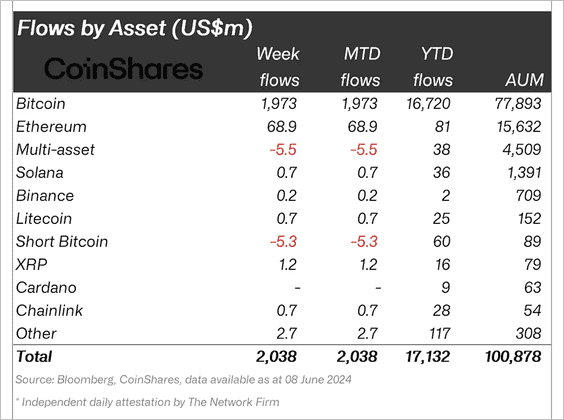

4. Crypto fund inflows accelerated last week, led by long-Bitcoin and Ethereum-focused products. (2 charts)

Source: CoinShares Read full article

Source: CoinShares Read full article

Source: CoinShares Read full article

Source: CoinShares Read full article

Back to Index

Commodities

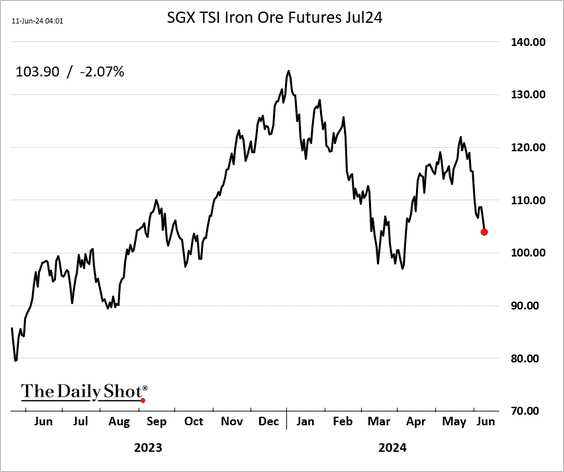

1. Iron ore futures keep moving lower.

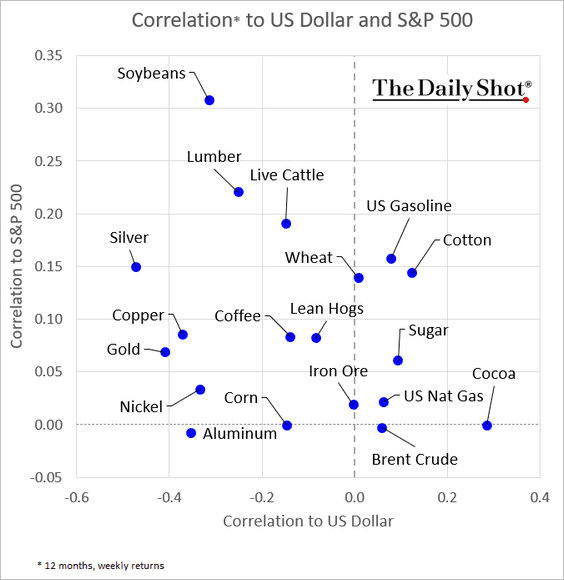

2. Here is a look at commodity markets’ correlations to the S&P 500 and the US dollar.

Back to Index

Energy

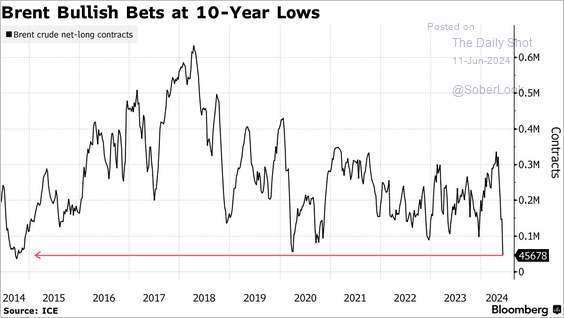

1. Speculative accounts keep reducing their bets on Brent crude.

Source: @markets Read full article

Source: @markets Read full article

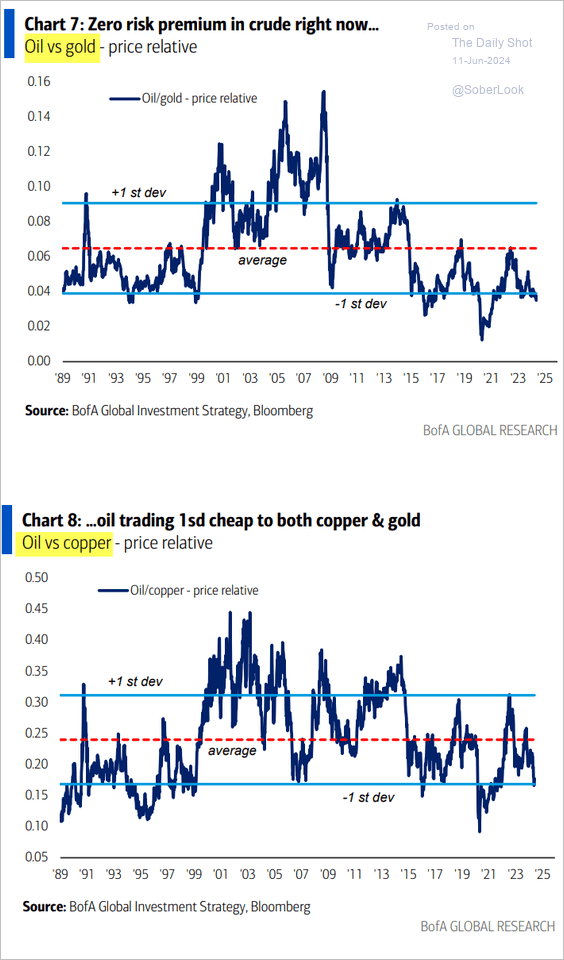

2. Here is a look at crude oil prices relative to gold and copper.

Source: BofA Global Research

Source: BofA Global Research

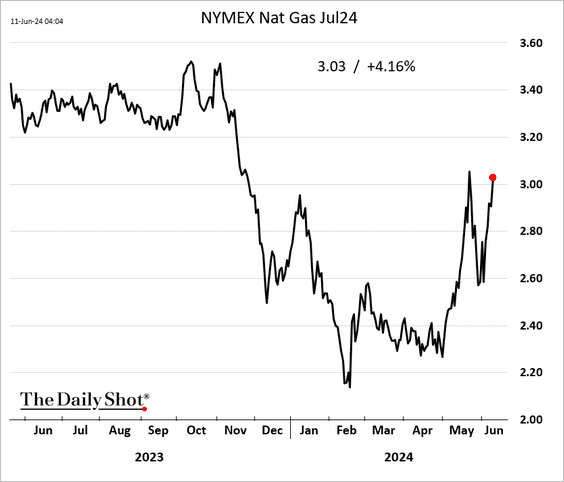

3. US natural gas futures are back above $3/mmbtu.

Back to Index

Equities

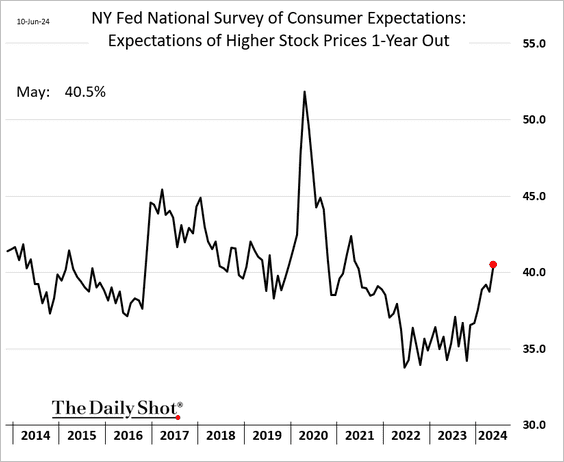

1. According to the NY Fed’s Survey of Consumer Expectations, US households are increasingly upbeat on stocks.

Source: @markets Read full article

Source: @markets Read full article

——————–

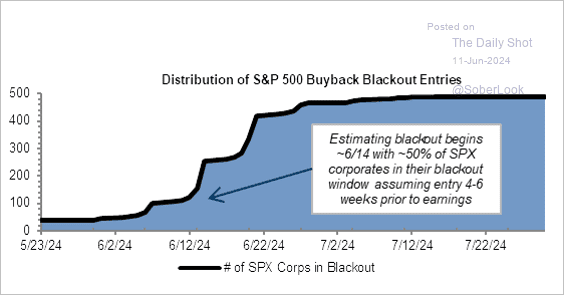

2. Share buyback activity is about to slow.

Source: Goldman Sachs

Source: Goldman Sachs

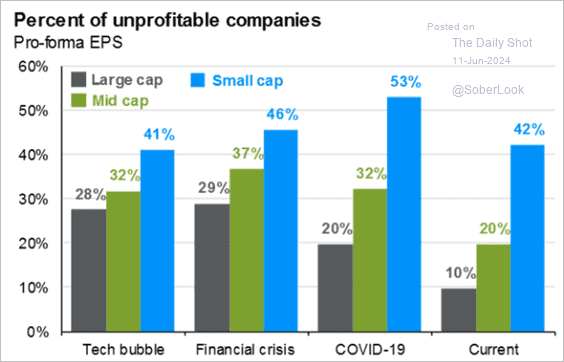

3. The percentage of unprofitable small-cap firms is unusually high.

Source: J.P. Morgan Asset Management

Source: J.P. Morgan Asset Management

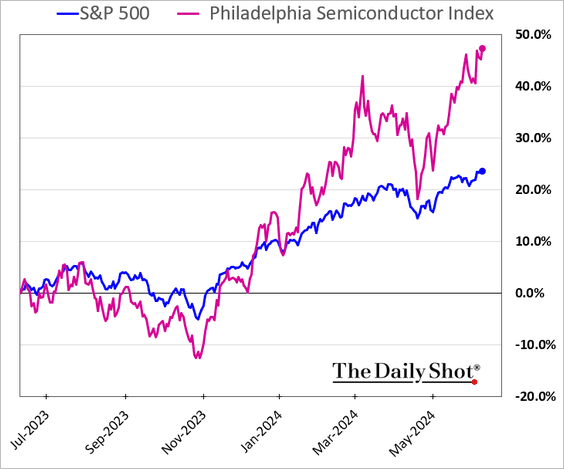

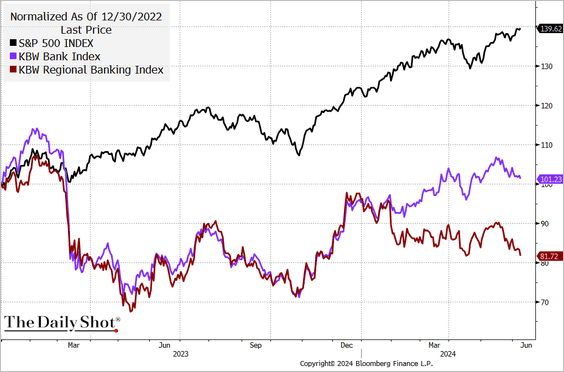

4. Next, we have some sector updates.

• Semiconductor stocks keep increasing their outperformance (driven by NVIDIA).

• Regional banks’ underperformance is widening.

Source: @TheTerminal, Bloomberg Finance L.P.

Source: @TheTerminal, Bloomberg Finance L.P.

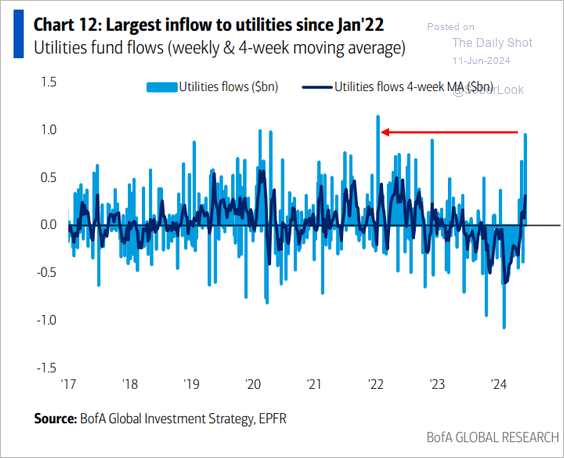

• Utilities are seeing substantial inflows.

Source: BofA Global Research

Source: BofA Global Research

——————–

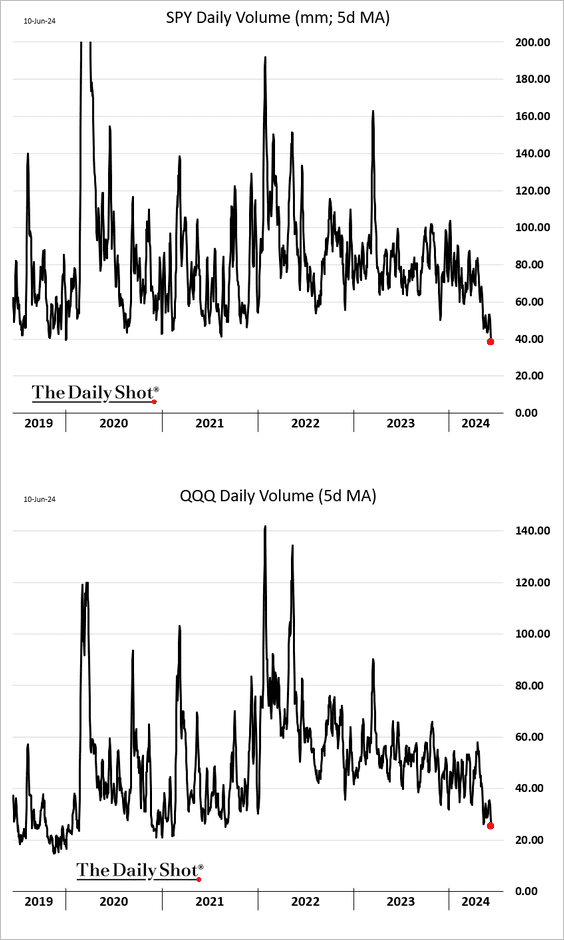

5. The most liquid US securities are becoming less liquid. Trading volumes for SPY and QQQ have been trending lower.

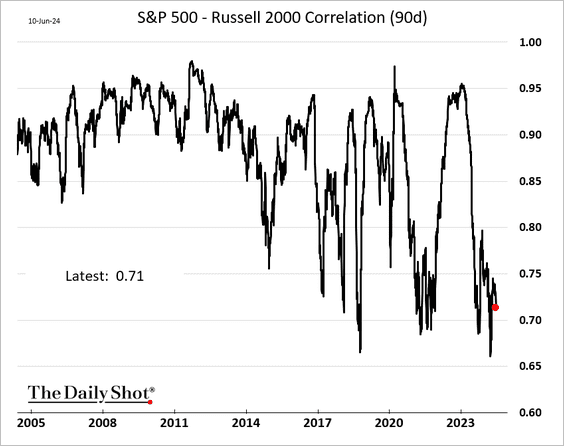

6. Small caps have been less correlated to large caps recently.

h/t @GunjanJS

h/t @GunjanJS

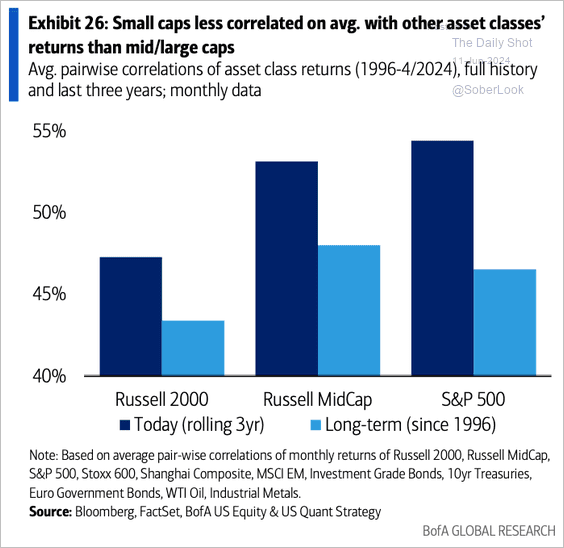

• Small caps are also less correlated with other asset classes.

Source: BofA Global Research; @dailychartbook

Source: BofA Global Research; @dailychartbook

——————–

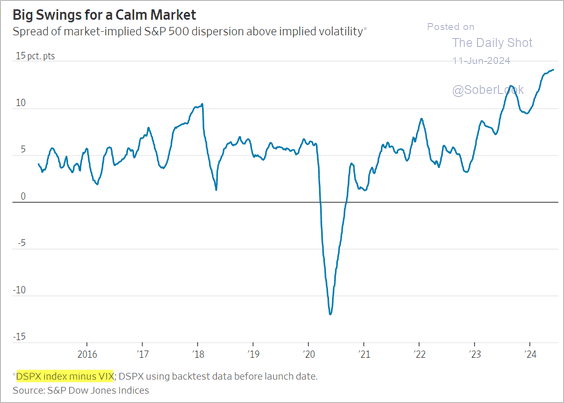

7. This chart shows the spread between the S&P 500 return dispersion and VIX.

Source: @WSJ Read full article

Source: @WSJ Read full article

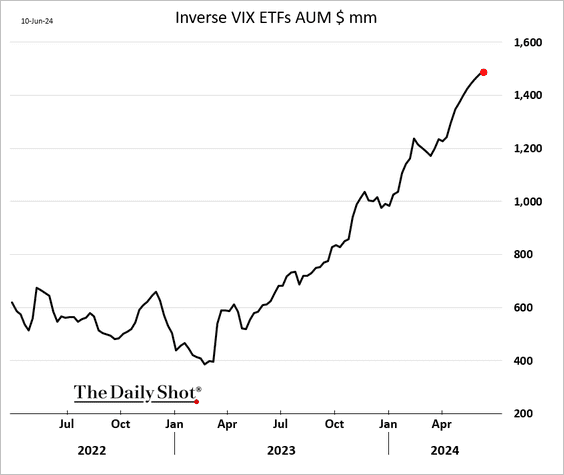

8. Inverse-VIX ETFs continue to see inflows. This is not going to end well.

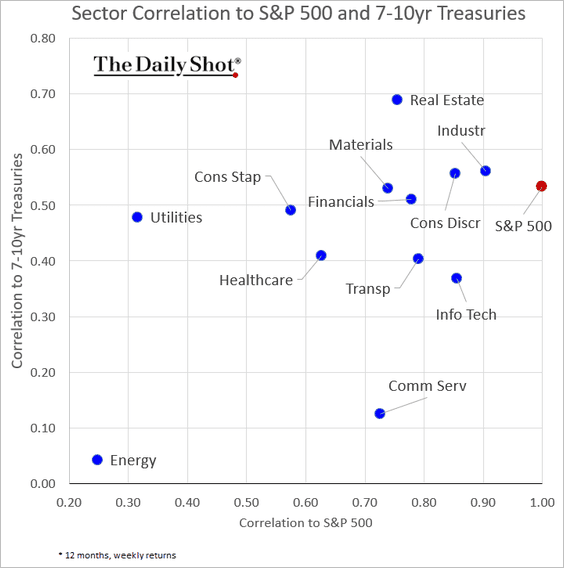

9. Finally, here is a look at the correlation of S&P 500 sectors to the S&P 500 and Treasuries.

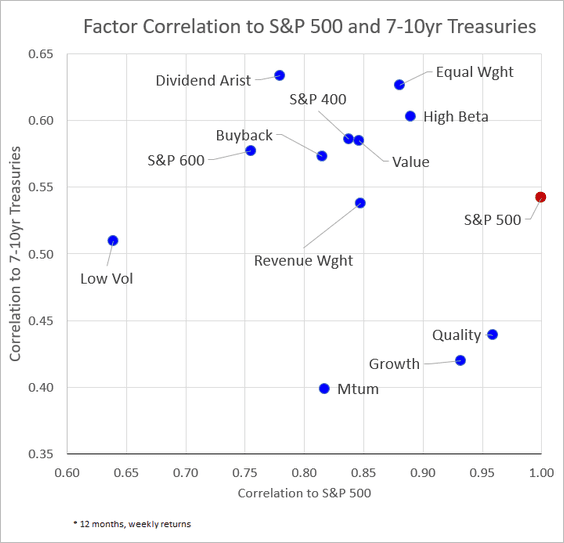

Below are the correlations by factor/style.

Back to Index

Credit

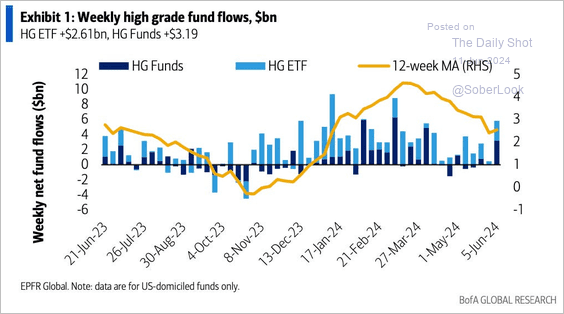

1. Investment-grade bond fund flows remain robust.

Source: BofA Global Research; @dailychartbook

Source: BofA Global Research; @dailychartbook

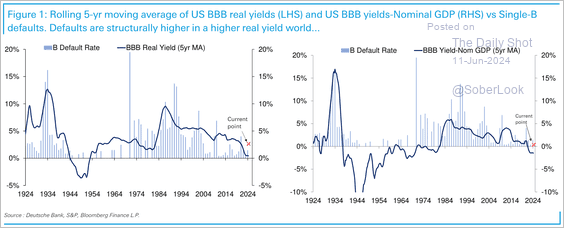

2. Deutsche Bank sees risk of higher US credit real yields and defaults, although not at extreme levels.

Source: Deutsche Bank Research

Source: Deutsche Bank Research

Back to Index

Global Developments

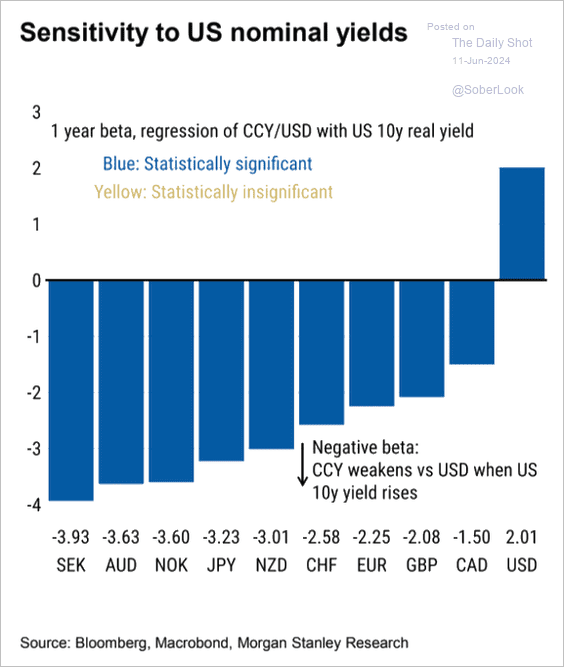

1. How do DM currencies respond to changes in US Treasury yields?

Source: Morgan Stanley Research; @AyeshaTariq

Source: Morgan Stanley Research; @AyeshaTariq

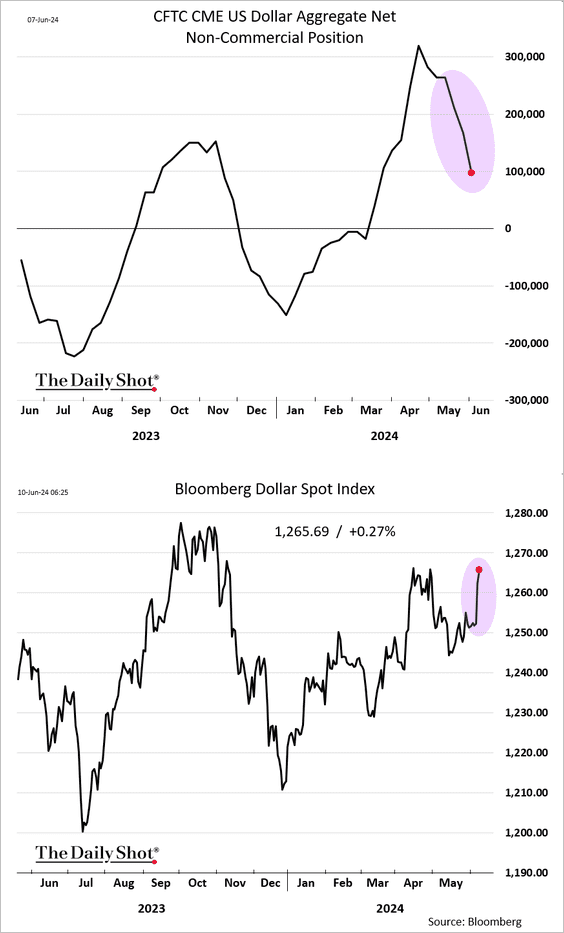

2. Speculative accounts have been cutting their US dollar exposure ahead of the rebound.

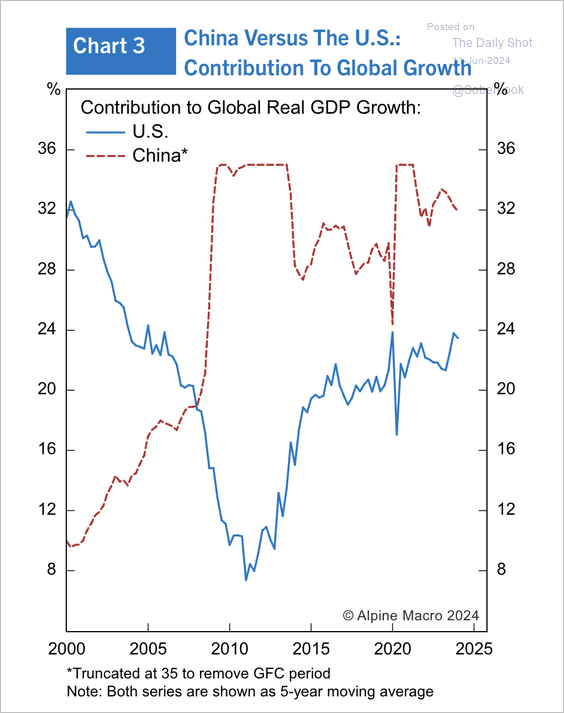

3. The US is contributing more to global growth as China stalls.

Source: Alpine Macro

Source: Alpine Macro

——————–

Food for Thought

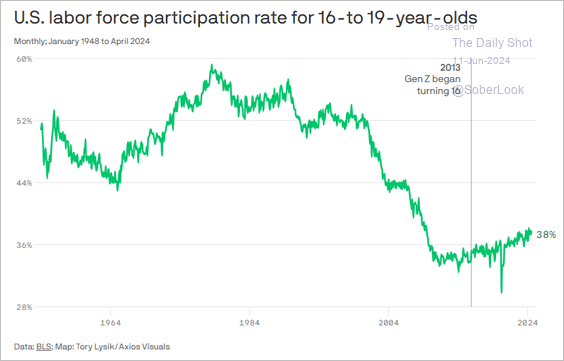

1. US teens’ labor force participation:

Source: @axios Read full article

Source: @axios Read full article

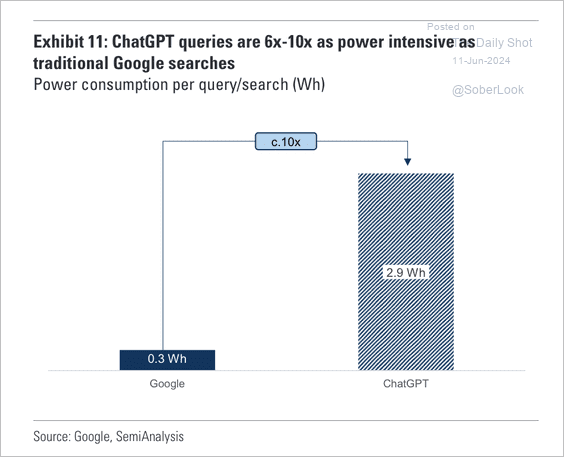

2. Marginal power consumption of ChatGPT vs. Google:

Source: Goldman Sachs

Source: Goldman Sachs

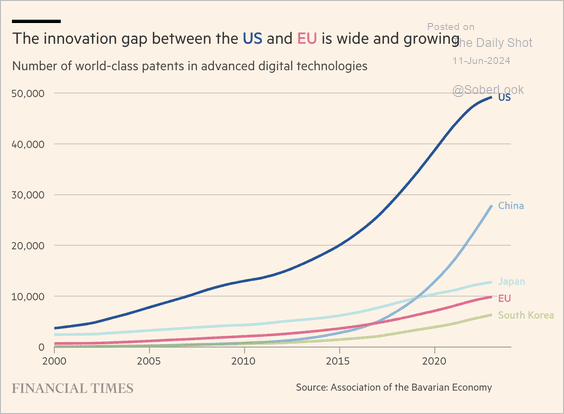

3. Advanced digital tech patents:

Source: @financialtimes Read full article

Source: @financialtimes Read full article

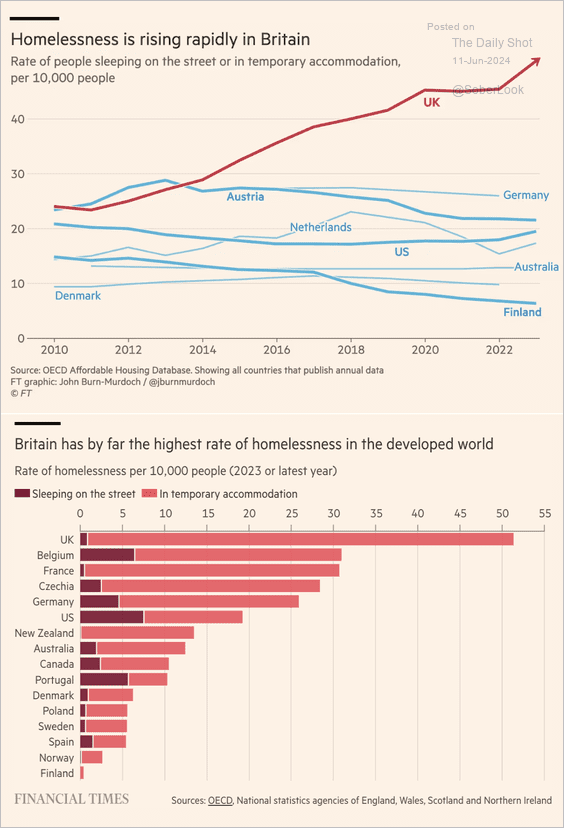

4. Homelessness in the UK:

Source: @financialtimes Read full article

Source: @financialtimes Read full article

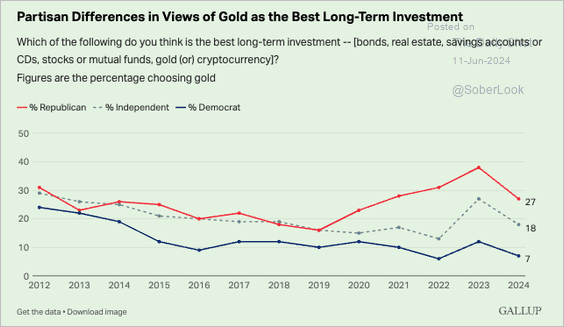

5. Views on gold as the best long-term investment:

Source: Gallup Read full article

Source: Gallup Read full article

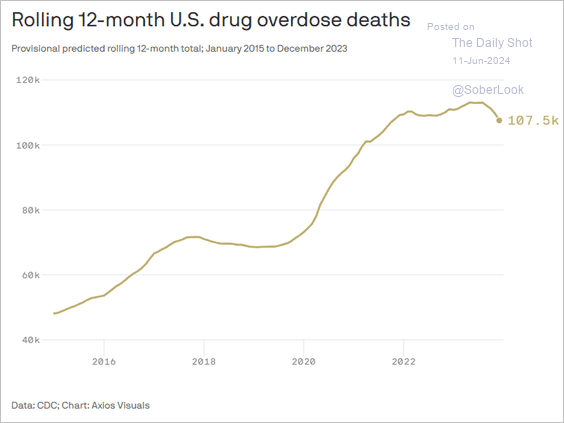

6. US drug overdose deaths:

Source: @axios Read full article

Source: @axios Read full article

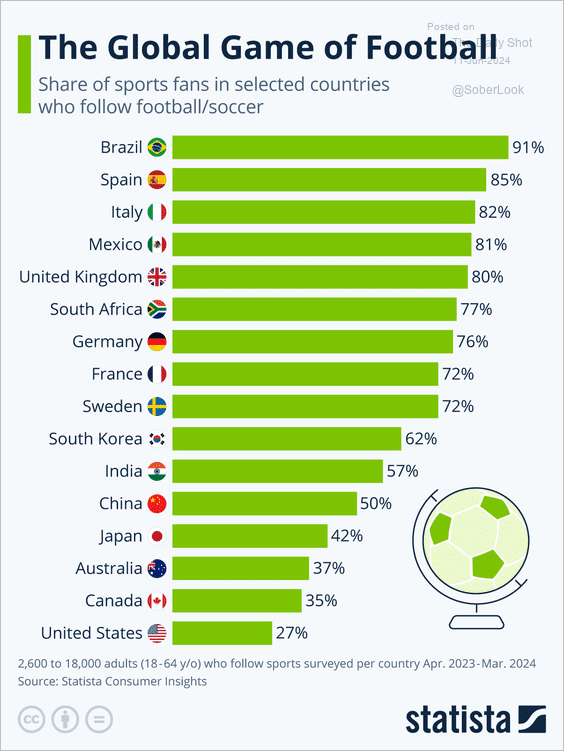

7. Global soccer fans:

Source: Statista

Source: Statista

——————–

Back to Index